Finland’s IQM Quantum Computers is moving to go public via a merger with Real Asset Acquisition Corp (RAAQ), valuing the firm at $1.8 billion and positioning it as the first European quantum hardware player to hit the open markets. This is not just another SPAC deal; it is a high-stakes stress test for a continent that has historically birthed world-class research only to watch the commercial profits migrate to Silicon Valley. By targeting a listing on the New York Stock Exchange and potentially a dual listing in Helsinki, IQM is attempting to bridge the gap between European engineering and American capital.

The math behind the $1.8 billion figure is aggressive. IQM reported approximately $35 million in revenue for 2025. This puts their valuation at a price-to-sales ratio north of 50. In any other industry, that would be laughed out of the room. In quantum computing, it is the price of admission for a company that has actually managed to move hardware out the door. While competitors like IonQ and Rigetti have faced the brutal reality of public market volatility, IQM is betting that its "full-stack" vertical integration—owning everything from the chip fabrication plant to the software layer—will provide the structural floor its predecessors lacked.

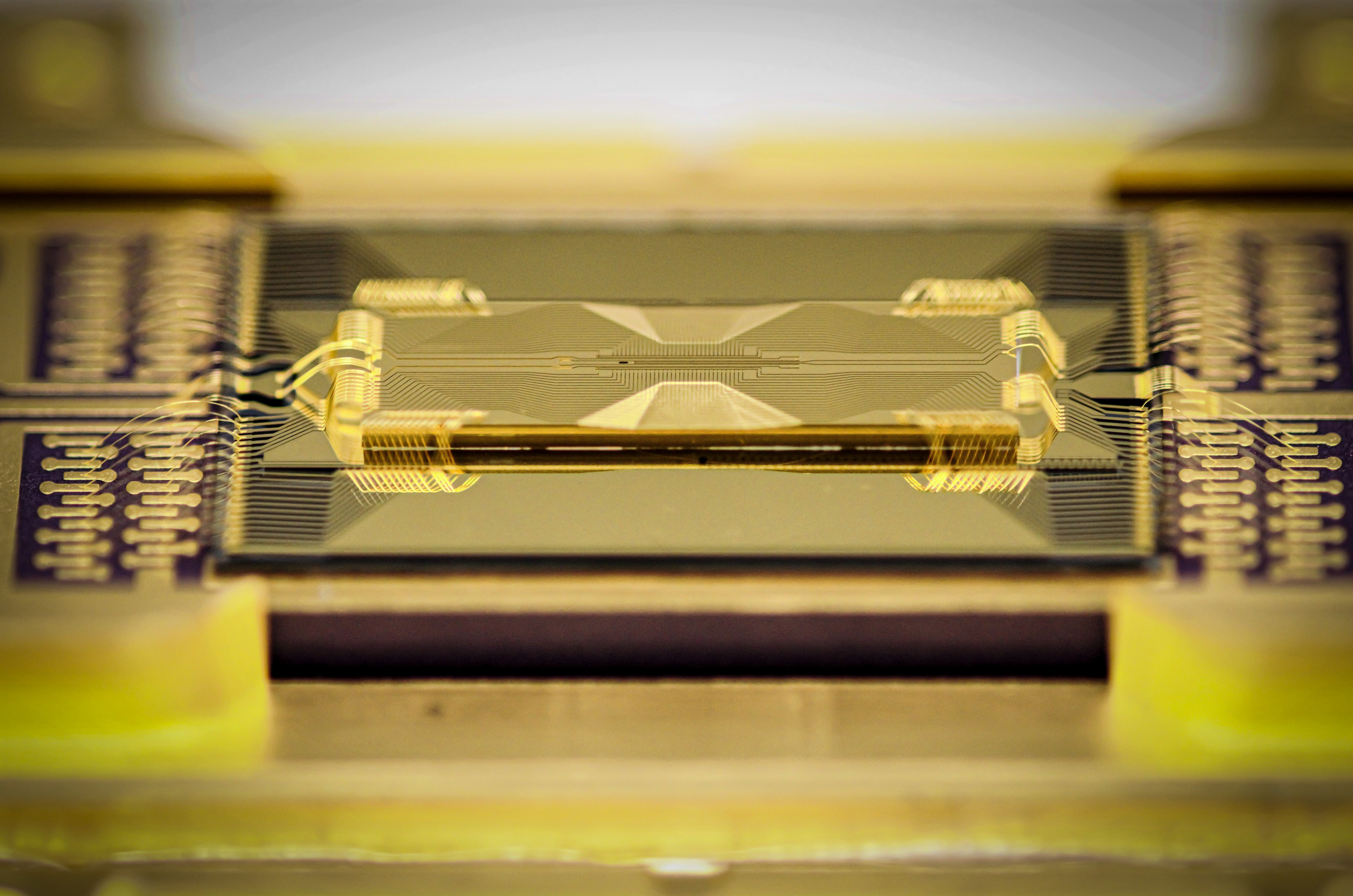

The hardware is finally leaving the lab

For years, quantum computing has been a "science project" funded by government grants and venture capital patience. IQM is trying to change that narrative by pointing to 21 systems sold and 15 delivered to date. These aren’t just theoretical blueprints. They are physical machines sitting in supercomputing centers like the Leibniz Supercomputing Centre in Germany, where the 54-qubit "Radiance" system recently went operational.

The company’s strategy avoids the "cloud-only" trap. While IBM and Google focus heavily on centralized quantum data centers, IQM has found a niche in on-premises deployments. National labs and security-conscious enterprises don't want their most sensitive algorithmic experiments running on a third-party server in another jurisdiction. By selling the box itself, IQM sidesteps the geopolitical anxieties of "quantum sovereignty" that currently dominate European policy.

Why the SPAC route still carries a scent of risk

The choice of a Special Purpose Acquisition Company (SPAC) in 2026 feels like a ghost from a previous era of exuberant finance. We all remember the 2021-2022 SPAC boom that left a trail of "de-SPAC'd" companies trading at 90% discounts. However, the structure of this deal suggests a more disciplined approach. The $450 million in expected cash at closing includes a $134 million PIPE (Private Investment in Public Equity) and $172 million already on the balance sheet.

Crucially, existing shareholders are locked in. There is no immediate cash-out for the founders or early backers, which is a necessary signal to the market that this is about growth capital, not an exit. The $450 million is intended to fund the "Halocene" platform, a next-generation system aimed at reaching the 99.9% fidelity threshold required for meaningful error correction.

The European sovereignty play

The European Union is currently obsessed with "technological sovereignty." The proposed EU Quantum Act of 2026 is designed to ensure the continent doesn't trade its reliance on US chips for a reliance on US quantum processors. IQM is the poster child for this movement. Headquartered in Espoo, Finland, it draws from a deep well of cryogenic expertise that traces back to the Aalto University Low Temperature Laboratory.

But staying European while listing in New York is a delicate balancing act. The talent is in Espoo, but the "deep pockets" required to survive the "quantum winter"—the period before fault-tolerant machines can break RSA encryption or revolutionize drug discovery—are in Manhattan. If IQM fails to maintain its valuation, it risks becoming a cut-price acquisition target for a US tech giant, the very outcome European regulators are desperate to avoid.

The 12 year roadmap vs the quarterly earnings cycle

The fundamental tension for IQM as a public company will be the timeline. Their own roadmap doesn't project true fault-tolerant computing until 2030 or beyond. Public markets are not known for their decade-long patience. They want to see that $100 million in bookings convert into realized revenue, and they want to see it fast.

The technical hurdles remain immense. Achieving 99.9% fidelity on a test chip is one thing; maintaining that performance across a thousand-qubit system is another entirely. Every time a competitor like IonQ announces a breakthrough in trapped-ion technology or Microsoft makes a leap in topological qubits, IQM’s superconducting approach will be called into question.

IQM is betting that being "first and real" in the European market is enough of a moat. They have the fab. They have the customers. They have the political wind at their backs. Now, they have to prove that a quantum company can survive the scrutiny of a balance sheet that classical investors can actually understand.

Watch the June 2026 closing date. If the redemption rates are low and the PIPE investors hold firm, IQM might just provide the blueprint for how European deep tech finally grows up.