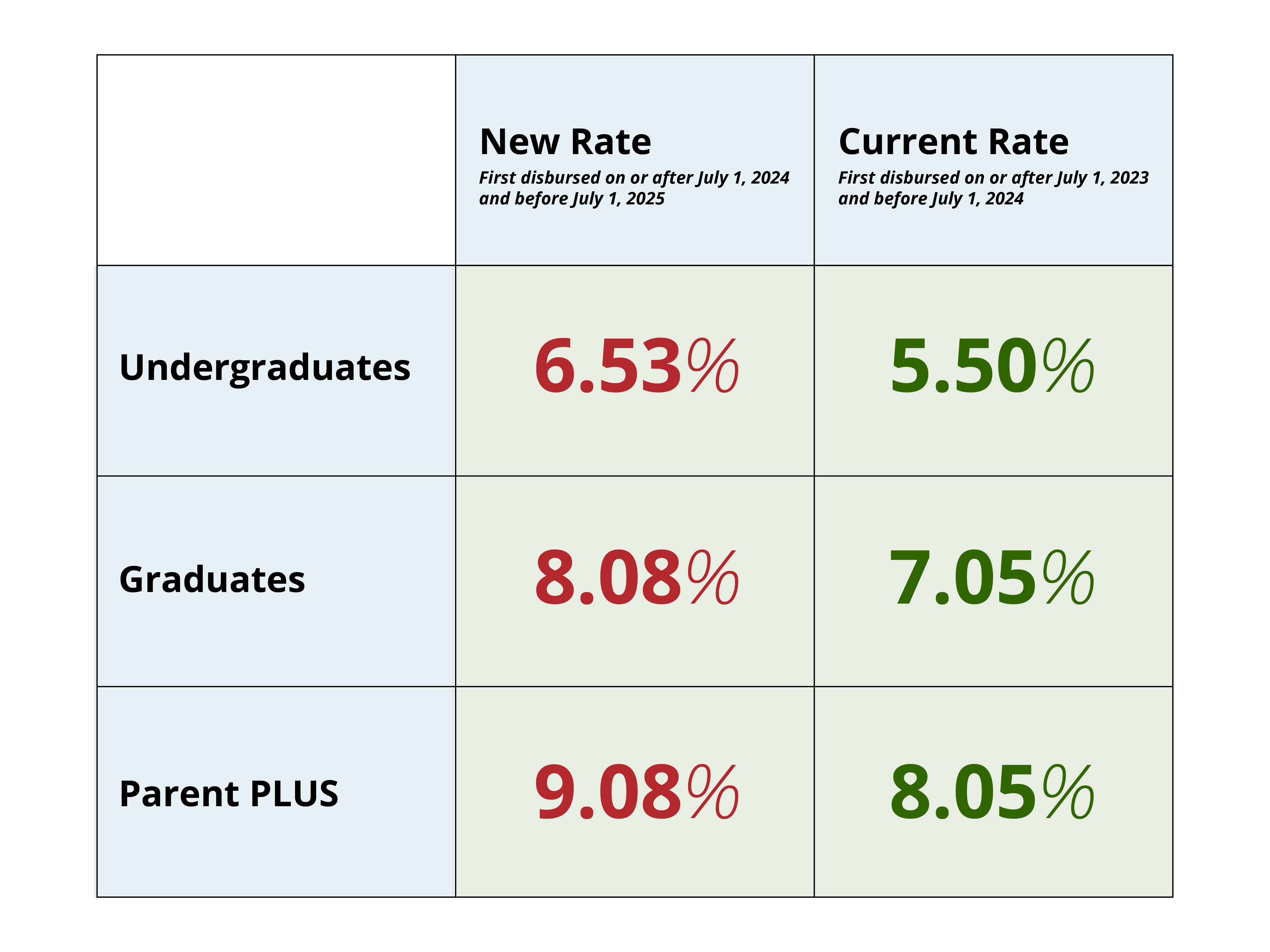

Stop panicking about the 2026-27 interest rate hikes. The financial press is feeding you a diet of pure, unadulterated fear because fear sells subscriptions. They want you to believe that a marginal uptick in the cost of borrowing is a death sentence for a generation. It isn't. In fact, if you’re smart, this rate hike is the best thing that could happen to your long-term net worth.

The lazy consensus says higher rates equal less opportunity. The "experts" look at the Federal Reserve's trajectory and the 10-year Treasury note—which dictates these student loan floors—and they see a crisis. I see a much-needed correction to a broken system that has encouraged students to overpay for mediocre degrees using "cheap" money.

When money is free, the price of the product goes up. When money gets expensive, the consumer finally starts asking if the product is actually worth it.

The High Cost Of Cheap Money

For a decade, we lived in a world of suppressed interest rates. This created a massive distortion in the education market. When the cost of borrowing is negligible, universities have no incentive to control tuition. They just hike the price because they know the federal government will underwrite the debt and the student won't feel the "burn" of the interest for years.

The 2026-27 rate hike is a signal. It’s the market finally telling you that a $200,000 degree in "Comparative Media Studies" from a mid-tier private college is a bad investment.

When rates rise, the ROI calculation changes. You are forced to become a venture capitalist of your own life. You have to look at your degree and ask: "Will this generate enough cash flow to cover a 7% or 8% cost of capital?" If the answer is no, you don't take the loan. You find a different path. Higher rates act as a filter for bad decisions.

The Myth Of The Debt Trap

The media loves the "debt trap" narrative. They’ll show you a spreadsheet where a $50,000 loan turns into $100,000 over twenty years. It looks terrifying on paper. But here is what they don't tell you: inflation is your silent partner.

If interest rates are rising, it’s usually because the economy is seeing persistent inflation. While your interest rate is locked in at the point of disbursement for federal loans, the value of the dollars you use to pay it back in ten years will be significantly lower.

Imagine a scenario where you borrow $30,000 today. In ten years, due to wage inflation, that $30,000 represents a much smaller percentage of your annual income. You are paying back "expensive" historical debt with "cheap" future dollars. The nominal interest rate is a distraction; the real interest rate—the nominal rate minus inflation—is often much lower than the headlines suggest.

Why You Should Ignore The Refinance Hype

Private lenders are salivating over these rate hikes. They’ll start hitting your inbox with "low-rate" offers to consolidate your federal debt. Don't do it.

I have watched people throw away the best insurance policy in the financial world just to save 1.5% on their interest rate. Federal student loans are not "normal" debt. They come with:

- Income-Driven Repayment (IDR) plans.

- Death and disability discharge.

- Public Service Loan Forgiveness (PSLF).

- Administrative forbearance options.

When you refinance with a private bank to chase a lower rate, you are trading those protections for a slightly smaller monthly payment. In a volatile economy, that’s a sucker’s bet. A private bank does not care if you lose your job. The federal government, through the SAVE plan or its successors, effectively acts as a backstop. That "high" interest rate is actually the premium you pay for a massive social safety net.

The Death Of The "Hidden" Degree Premium

We need to talk about the "credential inflation" that cheap loans fueled. Because everyone could get a loan, everyone got a degree. This devalued the bachelor’s degree to the point where it became the new high school diploma.

Higher interest rates break this cycle.

As the 2026-27 rates kick in, we will see a shift toward trade schools, certifications, and "earn-while-you-learn" models. This is a win for the individual. If you can enter the workforce as an electrician or a specialized technician with zero debt while your peers are sweating over 8% interest on a philosophy degree, you haven't just won the financial game—you’ve lapped the field.

Stop Asking "How Much Can I Borrow?"

The premise of the current "expert" analysis is flawed. They focus on how students can afford the higher rates. This is the wrong question.

The right question is: "How can I avoid borrowing this money entirely?"

The rising rates are a wake-up call to look at the alternatives that were ignored during the era of easy money:

- The 2+2 Strategy: Two years of community college at near-zero cost, then transferring to a state school. The diploma looks exactly the same, but your debt load is slashed by 60%.

- Employer-Sponsorship: More companies are paying for degrees upfront to secure talent in a tight labor market. If they won't pay for it, it’s a sign they don't value the credential.

- The "Gap Year" Arbitrage: Work for a year. Save. Understand what you actually want to do. The maturity gained often leads to finishing a degree faster, which is the ultimate interest-rate hedge.

The Brutal Reality Of Compounding

I won't lie to you: interest is a beast. If you carry a balance for thirty years, you are making the Department of Education very wealthy. But the "scary" new rates only matter if you treat your student loan like a permanent tax.

If you treat it like a business debt—something to be leveraged for a high-income skill and then liquidated as fast as humanly possible—the interest rate is almost irrelevant. A 2% difference in interest doesn't matter if you pay the loan off in four years instead of twenty-five.

The people crying about 2026 rates are the ones who plan to pay the absolute minimum for the rest of their lives. That’s not a debt problem; that’s a math and discipline problem.

The Meritocracy Returns

For too long, the student loan system functioned as a subsidy for the wealthy and a burden for the middle class. Wealthy parents paid cash; the middle class took the "cheap" loans and got squeezed.

With higher rates, the "prestige" of certain expensive institutions will begin to crumble. When a degree at a top-tier private school costs $90,000 a year and the interest rate is 8%, the math stops working even for the upper-middle class. You will see a flight to quality and value. State schools will become more competitive, and their brands will strengthen. This levels the playing field.

[Table: Cost vs. ROI Comparison of State vs. Private Universities in a High-Interest Environment]

| Variable | State University (Commuter) | Private "Prestige" College |

|---|---|---|

| Annual Tuition | $11,000 | $65,000 |

| Interest Accrual (7%) | $770/yr | $4,550/yr |

| Total Debt (4 years) | $44,000 | $260,000 |

| Monthly Payment (10yr) | ~$510 | ~$3,000 |

Look at those numbers. The higher the rate, the more devastating the gap becomes. The "prestige" college isn't six times better than the state school. It’s just six times more expensive. The 2026 rate hike makes this reality impossible to ignore.

Leverage The Panic

While everyone else is complaining about the rising rates, use this as your moment to negotiate.

Universities are terrified of declining enrollment. They know that higher interest rates make their "sticker price" look insane. This gives you, the student/parent, more leverage than you’ve had in twenty years. Appeal the financial aid package. Ask for merit scholarships. Demand a better deal.

The "experts" want you to feel like a victim of macroeconomic forces. I'm telling you to be the predator. Use the high-rate environment to justify why you won't pay full price.

The Bottom Line

A student loan is a tool. In a low-interest environment, people used that tool like a hammer on every problem they had. Now that the tool is getting more expensive and sharper, you have to use it like a scalpel.

Don't fear the rate hike. Respect it. Let it talk you out of bad investments. Let it force you into a higher-paying career path. Let it drive you toward aggressive repayment.

The people who will struggle in 2026 are those who continue to act like it's 2015. They will borrow blindly, pay slowly, and complain loudly.

You? You'll look at the 8% interest rate, decide the degree isn't worth the squeeze, and find a way to get the same education for ten cents on the dollar.

The "crisis" is only for people who can't do math. For everyone else, it's the start of a much-needed era of financial sanity.

Stop looking for a lower rate and start looking for a higher ROI.

:strip_icc()/white-farmhouse-flowers-porch-a5a1b33f-3d06de2580894c4bb6587c34a4823a9b.jpg)